By: Impana Halgeri and Bokka Ashwika

Introduction

The control over mergers and amalgamations exercised by competition law is a fascinating new avenue that developing countries have recently begun exploring. With most developing nations now having competition law regimes, it becomes important to discuss what perspectives on competition policy may be taken by these nations.[1] India introduced the Green Channel Route as an automatic combination approval mechanism in August 2019.[2] Since then, 25% of all applications to the Competition Commission of India (hereinafter, CCI) regarding combinations have gone through the Green Channel Route.[3] In light of this, it is important to examine the implications that such a channel has on Indian competition policy and compare whether the introduction of such a channel is at par with international practices in developing countries regarding mergers and amalgamations.

In order to do this, this essay unfolds in four parts. In Part I, the current Indian competition law regime regarding combinations is analysed, which is inclusive of the working and shortcomings of the Green Channel Route. In Part II and III, a glance at the competition law regime in South Africa and Brazil is taken consecutively to give a brief background regarding the context with which the readers may analyse the main part of the essay. Part IV expounds the central idea of the essay which is regarding what India can learn from the aforementioned jurisdictions in order to create a more holistic and less vague Green Channel Route. Additionally, reasons as to why South Africa and Brazil in particular were chosen are also discussed. Finally, the essay concludes by giving some suggestions to implement the lessons learnt from the aforementioned jurisdictions.

I. The Indian Competition Regime And The Regulation Of Combinations

Indian competition law gained traction when the Monopolies and Restrictive Trade Practices Act (hereinafter, MRTP Act) was enacted in 1969.[4] Later, this Act was repealed as India steadily advanced along the path of reforms that included liberalisation, privatisation, and globalisation.[5] In light of the Raghavan Committee report, the Competition Act of 2002 was enacted.[6] This Act has undergone many amendments, the latest one being the Competition (Amendment) Act, 2023.[7] The new amendments are meant to be read with reference to the principal Act.[8] Merger control policies are also regulated by notifications published under the Ministry of Corporate Affairs[9] and the CCI (Procedure in regard to the transaction of Business relating to Combinations) Regulations, 2011 as amended by the Amendment Regulations, 2019.[10]

The CCI was established to meet the objectives of the Act.[11] The CCI consists of a Chairperson; six members appointed by the Central Government[12] and a Director General.[13] This Commission has the power to enquire about combinations which are likely to cause adverse effects on competition in India.[14] The general test used by the authority to ascertain if a combination should be allowed is the ‘Appreciable Adverse Effect on Competition’ test or the ‘AAEC test’. Section 20(4) of the Act expounds the factors upon which CCI determines whether the given combination is likely to cause adverse effects on competition.[15] If a combination is likely to cause adverse effects on competition, such combination shall be void.[16]

A. The Normal Route:

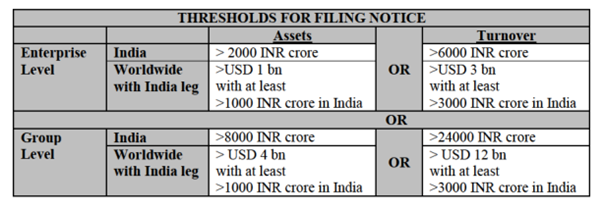

Thresholds & Notification: Section 5 of the Act defines combination as ‘the acquisition of one or more enterprises by one or more persons or merger or amalgamation of enterprises shall be a combination of such enterprises and persons or enterprises’.[17] This section also gives thresholds for enterprises to notify CCI as follows:[18]

Source: Competition Commission of India

The 2023 Amendment bought in the ‘Deal Value Threshold’. According to this, if the ‘value of any transaction exceeds rupees two thousand crores and the enterprises have substantial business operations in India as may be specified by regulations,’[19] the parties must notify CCI. The 2023 Amendment to the Act, removed the 30 days time limit for filing a notification.[20] A notification of combination is filed to CCI by submitting either Form I (shorter form) or, if the parties involved have a market share that is more than 15% horizontally overlapping and a market share that is more than 25% vertically overlapping, Form II (longer form).[21]

Procedure: According to Section 6 of the Act, ‘no combination can come into effect until 150 days have passed from the day on which the notice has been given to the Commission’.[22] The first step of the procedure involves the CCI forming a prima facie judgement on whether a combination would have a materially adverse effect on competition in India within 30 working days of receiving notification from the parties. An additional 15 working days are provided to the CCI in situations wherein it contacts third parties under Regulation 19 of the Combination Regulations to examine the impact of a transaction.[23]

If the CCI believes that an AAEC exists, it issues notice under Section 29 of the Act and gives a chance to the parties to make their case as to why a thorough investigation to determine the merger’s competitive effects should not be conducted.[24] After hearing them, if parties accept CCI’s suggestions then CCI may approve the transaction.[25] If the issues are not solved, it may also direct the Director General to conduct an enquiry regarding the same.[26] If the commission does not pass an order or issue directions within 150 days, it can be presumed that the commission has given approval for the combination.[27]

B. The Green Channel Route:

After the recommendations made by the ‘Report of the Competition Law Review Committee’, the Competition Commission of India (Procedure in regard to the transaction of business relating to combinations) Regulations, 2011 was amended to add an automatic system of approval for combinations through a ‘Green Channel Route.’ This was done in consideration of the needs of the market and best practices in other jurisdictions.[28]

Subject to the Commission’s determination that the combination comes under the ‘Green Channel’ scheme, a combination is presumed to have been accepted upon filing the notice in the required format and acknowledging its receipt. The time and cost of transactions would be greatly reduced by this method. Parties may opt for this if the combination is not causing AAEC.

The 2019 Amendment to the Regulations added Regulation 5A, Schedule III, and Schedule IV.[29] The method outlined in Regulation 5A allows the parties to a combination to submit notice via Form I, in accordance with Regulation 5, if it falls under the definition of a combination as stated in Schedule III.[30] The declaration listed in Schedule IV must also be enclosed with the aforementioned notice. After the notification is made, if the parties receive the receipt of acknowledgement by the Commission, then the combination is deemed to be approved.[31]

The Competition (Amendment) Act 2023 formally added the Green Channel Route to the Act. If the entities that filed for combination have no horizontal, vertical, or complementary overlap, then it is deemed to be approved by the Commission from the date of application.[32] The amendment substituted Section 5(4)[33] and Section 5(5)[34] of the Act.

Although the green channel has been beneficial in many ways, it is lagging behind with respect to its implementation in India. As certain criteria prescribed by the CCI as to what transactions come under the Green Channel Route are vague, parties to the combination have no clear idea of what satisfies the criteria under this process.[35] The CCI gave clarity in notes to Form I that, if problems arise, it may declare the combination void ab initio and have a right to start proceedings against them according to Section 44 of the Act for ‘gun jumping’.[36] This may discourage parties from filing under this Route.

Another major problem is there is no deadline set for the CCI to decide if a combination is ultimately not appropriate for the Green Channel route. As a result, parties will need to submit a brand-new notification, and if they have already consummated the transaction by that point, they may be held accountable under section 44 of the Act and section 43A.[37] Parties may be hesitant to pursue the Green Channel option because of the uncertainty around the CCI’s turnaround time.[38] Hence, it can be inferred that filing under the Green Channel Route comes with certain disadvantages.

II. A Glance At Merger Control In South Africa

Africa is a developing continent which is bringing in billions in investments every year.[39] Due to this increase in business, it has become important for Africa to have a vigilant competition law regime in place. South Africa is a fascinating example of competition law enforcement in a developing nation. The merger control regime in South Africa is governed by the Competition Act 89 of 1998, as amended from time to time.[40] It pertains to any economic activity occurring inside or having an impact on South Africa.

The preamble to the Act mentions that the purpose of the Act is to provide a Competition Commission that is in charge of investigating, controlling, and evaluating restrictive practices, abuse of dominant position, and mergers.[41] Additionally, the preamble also mentions the setting up of a Competition Tribunal which is responsible for the adjudication of such matters.[42] Additionally, the Competition Appeal Court is also a relevant body.[43]

The hierarchy between these bodies may be understood thusly:[44] Following an examination, the Competition Commission authorises or forbids certain small and all intermediate mergers. In the case of large mergers, the Commission advises the Competition Tribunal on whether the combination should be approved or prohibited. The Competition Appeal Court hears appeals from the Tribunal.

A. Thresholds & Notification:

Section 12 of the Act defines a merger as ‘the direct or indirect acquisition or direct or indirect establishment of control by one or more persons over all significant interests in the whole or part of the business of a competitor, supplier, customer or other person.’[45] Mergers are classified into three types: small, intermediate and large.[46] A merger is classified as intermediate if the proposed merger’s worth equals or surpasses R600 million (determined by combining the annual turnover of both businesses or their assets), and the target firm’s annual turnover or asset value is at least R100 million. Any mergers that fall below this threshold are considered as small mergers. If the combined annual revenue or assets of the acquiring and target firms are valued at or above R6.6 billion, and the target firm’s annual turnover or asset value is at least R190 million, the merger is considered to be a large one.[47] Intermediate and large mergers must be notified to the Competition Commission before they are implemented.[48]

B. Procedure:

The Commission has a maximum of 60 working days to consider and deliver a final decision on intermediate mergers.[49] If no decision is made within this time frame, the merger is considered authorised. In the case of large mergers, the Commission has 40 business days to assess the transaction and submit a recommendation to the Tribunal.[50] With the cooperation of the parties or the Tribunal’s approval, this term can be extended by up to 15 working days at a time. In a large merger inquiry, there is no limit to the number of extensions that can be granted. The Tribunal must render its final judgement within ten business days of receiving the suggestion and within ten business days of the hearing’s conclusion.

The general test used by these bodies for determining if a merger should be allowed or not is the ‘substantially prevent or lessen competition’ test or the ‘SLC’ test. Here, the factors involved are in Section 12A(2) of the Act, such as ‘the actual and potential level of import competition in the market’ and ‘the ease of entry into the market’.[51] Another interesting consideration taken up in the South African merger review process is the ‘Public Interest Considerations’ or ‘PICs’, which will be further discussed in Part IV.

III. A Glance At Merger Control In Brazil

For many decades in Brazil, competition law played a very minor role, especially in mergers and price controls. Competition law took a new form in the Brazilian economy in 1994 when Federal Law (8.884/94) was enacted which contained merger control policies.[52] Presently, the merger control regime is regulated by The Competition Act of 2022 (Law No. 14.470/2022) which amended the Competition Act (Law No. 12.529/2011).[53] This Act has an effect on entities inside the territory of Brazil as well as foreign entities that have transactions or branches in Brazil.[54]

Conselho Administrativo de Defesa Econômica (hereinafter, CADE)[55], the competition authority in Brazil, was established in 1962. It is an adjudicatory body under the Ministry of Justice.[56] The goal of CADE is to guarantee fair competition. CADE is divided into three bodies:[57]

- Administrative Tribunal of Economic Defence;

- General Superintendence(GS); and

- Department of Economic Studies.

Firstly, the General Superintendence Office (hereinafter, GS) is headed by the Superintendent-General of CADE and this office is responsible for assessing all transactions filed for merger control and clearing those that can be granted without CADE’s interference.[58] Secondly, the Administrative Tribunal of Economic Defence has the power to deny merger transactions and make decisions regarding complicated merger cases that call for remedies or have been the subject of third parties’ appeals. This authority also has a right to review the decision given by GS. Finally, the Department of Economic Studies is led by the Chief Economist of CADE and this consulting body is tasked with creating economic studies and providing non-binding economic conclusions at the request of the Superintendent-General and the commissioners of the Administrative Tribunal.[59]

A. Thresholds & Notification:

In Brazil, the thresholds for the notifications depend on the gross revenues of the parties for the year prior to the proposed transaction. These thresholds can be seen below:[60]

“Art. 88. The following shall be submitted to CADE by the parties involved in the operation of acts of economic concentration in which, cumulatively:

I – at least one of the groups involved in the transaction has registered, in the last balance sheet, annual gross sales or total turnover in the country, in the year preceding the transaction, equivalent or superior to four hundred million reais (R$ 400,000,000.00); and

II – at least one other group involved in the transaction has registered, in the last balance sheet, gross annual sales or total turnover in the country, in the year preceding the transaction, equivalent to or greater than thirty million reais (R$ 30,000,000.00).”

If a merger is meeting this threshold, then a mandatory notification is needed. Even if a transaction does not fully satisfy the criteria for required filing, CADE may nonetheless decide to submit it for review up to a year after the deal is finalised.[61]

B. Procedure:

The GS first reviews the papers presented by the parties. A public notice is published in the Official Journal whenever the GS determines that the notification is supported by all the data required to begin the analysis.[62] Depending on the intricacy of the transaction and the requirement for more information, the GS’s deadline for making a final decision varies.[63] There are two possible outcomes of GS’s evaluation. Firstly, it may be unconditional approval by giving another public notice in the Official Journal.[64] In this case, an appeal may be filed against the decision of GS within 15 days.[65] This appeal is made to the Tribunal by any interested party. Secondly, GS may present it to the Tribunal to take a final decision.[66]

There are two procedures followed by the CADE in case of mergers. Firstly, in case of the normal procedure, a final administrative decision must be issued within 240 days of being notified, according to the Competition Act’s statutory time limits for reviewing transactions.[67] Secondly, there exists a fast-track process for merger approvals.[68] In such cases, a final decision is made within 30 days after filing by the CADE.[69] This process will be further discussed in the Part IV.

Generally, in the Brazilian competition regime, the CADE rejects mergers if the operation has a chance of creating dominance or suppressing the competition which might affect the market as a whole or creates market dominance.[70]

IV. A Cross Jurisdictional Analysis Of Merger Policies: Deficiencies In The Green Channel Route

Merger control in developing nations is an often debated topic in Competition law discourse. This is because effective competition policy is empirically proven to be beneficial for the growth of developing economies, since increased competition policy implementation leads to the expansion of more efficient private enterprises.[71] Hence, it is important to understand how developing economies can be benefitted from specific approaches to competition law policy.

It has been argued that competition policy in developing nations like India should incorporate a voluntary framework, in which merging parties have the choice, but not the requirement, to have their transaction examined by competition authorities.[72] This is because most industries in India are fragmented and hence monopolies or oligopolies may have to be tolerated in order for economic structures to be more efficient, and it may be wiser to shift the attention to remedies for specific behaviour rather than restricting ‘size’ per se.[73]

However, in the last decade, it can be noted that Indian competition law did not go down the aforementioned route and rather opted for a more vigilant policy, with notifications being mandatory for combinations that breach a certain monetary limit.[74] Besides, if monopolies and oligopolies are tolerated within an economic system, the very essence and purpose of competition law is lost. Therefore, this essay argues for a robust competition law system within which the interests of all stakeholders in a competing economy can be accommodated. In order to do this, examples from other jurisdictions, namely, South Africa and Brazil, may be analysed.

A. Why South Africa and Brazil?

Before understanding what India can learn from South Africa and Brazil, it should first be understood why South Africa and Brazil were chosen. With all three countries being a part of the BRICS (Brazil, Russia, India, China and South Africa) alliance, they are thought to be amongst the most prominent emerging economies in the world. BRICS is an important association that brings together the world’s main emerging economies, accounting for 41% of the world’s population, 24% of global Gross Domestic Product, and more than 16% of global trade.[75] Analysing the merger policies of two fellow BRICS countries will allow India to further its own economic capabilities while being measured at the same level and within the same context as other comparable developing nations.

This essay rejects the absolutist view that competition policy should be similar in all jurisdictions.[76] Competition law in developing countries takes on a whole new perspective as markets do not work as well as they do in developed economies.[77] Inequality of wealth, power, and economic opportunity is widespread and frequently recognised as causing difficulties that all legal disciplines must address.[78]

Therefore, due to the distinct problems faced by developing economies when compared to developed economies as well as the comparable nature of South Africa, Brazil and India’s economies, these countries were chosen as the basis of comparison.

B. South Africa, Competition Law and Public Interest Considerations

As has been discussed above, the SLC test was developed in response to the economic consequences of mergers and the need to safeguard competition. The socio-economic and socio-political impact of mergers on people, on the other hand, led to the establishment of the PIC test.[79]

Public interest is notoriously difficult to define. However, Section 12A(3) of the Competition Act lays down the criteria that the deciding authority must consider when analysing if the merger can or cannot be justified on the grounds of public interest.[80] The considerations set forth involve analysing if the merger has a substantial impact on: a specific industrial region; employment; the capacity of small and medium-sized enterprises to participate or develop in the market successfully (especially firms owned by historically disadvantaged people); the ability of national industries to compete in international markets; and if the merger increases the levels of ownership by historically disadvantaged people.[81]

The Competition Act makes it unlawful to merge if the combination will significantly reduce competition (SLC).[82] If a merger fails this standard, it will be evaluated under the PIC test to see if other pro-competitive advantages, such as technical innovation or efficiency, can compensate for it failing the SLC test. Hence, if the merger passes the PIC test, it will be allowed. However, in reality, no merger has been approved for merely passing the PIC test.[83] Rather, mergers that pass the SLC test but still raise substantial public interest considerations are given conditions for approval of the merger. For example, in the case of the merger between Walmart Stores Inc. and Massmart Holdings Ltd., the Commission allowed the merger between the two entities with some conditions such as ensuring that there are no retrenchments based on Massmart’s operational requirements for a period of at least two years from the date of transaction as well as ensuring that when employment opportunities become available within the merged entity, preference will be given to the re-employment of the employees that were retrenched during an earlier period.[84]

C. Public Interest Considerations, Indian Competition Policy and the Green Channel Route

Factoring in public interest considerations is not new to Indian competition policy. In fact, the MRTP Act listed specific circumstances which could rebut the presumption that a certain restrictive trade practice was against public interest.[85] The new Competition Act, 2002 interacts with public interest concerns in a relatively vague manner. The Act was enacted keeping in mind the ‘economic development of India’ which is dependent entirely on the Commission’s subjective interpretation of the word ‘development’ and could potentially include public interest considerations.[86] It may also be used to exonerate anti-competitive activities of large corporations done under the guise of development.[87]

Additionally, the new Act also includes Sections 21 and 21A which may allow for the coordination of competition policy with the public interest.[88] Section 49, which deals with advocacy, adds another platform for protecting public interest.[89] Furthermore, under Section 54, the government has the ability to exclude sectors and industries from competition legislation.[90] It must be noted that neither of these Sections include the phrase ‘public interest’ and it is only hypothetical that such Sections may be used to address public interest concerns. In fact, there has been recent discourse that the decisions of the CCI have been shifting their focus away from public interest, especially in the case of platform markets.[91]

It may be argued that the Green Channel Route is another step away from analysing mergers and amalgamations in the context of public interest. As has been discussed earlier, in order to get combinations approved under the Green Channel Route, the parties must file a Form 1 application. Public interest concerns have not been accommodated in any of the questions that are to be answered when filing a Form 1 application.[92] This allows for combinations that raise considerable public interest concerns to be allowed through the Green Channel Route. As these combinations are ‘deemed to be approved’ if they meet certain criteria, the Commission does not interact with these transactions enough to understand their impact in a holistic manner.

D. Brazil, Competition Law and Fast-Track Procedure

As has been discussed above, for simpler transactions, fast-track procedure is implemented by Brazilian CADE under Resolution No. 16/2016. These transactions mainly involve mergers which cause little or no harm to the competition regime.[93] In this procedure, the information to be provided is minimal and the procedure is simpler when compared to the normal procedure.[94]

Regulation 33/2022 of CADE furnishes six criteria that a merger has to satisfy to come under the fast-track procedure. For example, combined market share, to a certain extent, in case of horizontal and vertical overlapping is allowed.[95] With this demarcation, the merging entities will have a clear idea regarding whether this procedure applies to them or not.

The 2016 resolution of CADE elaborates that when a merger is filed under this procedure, the GS must give the decision within 30 days of filing the same. After the approval for the combination, the companies have no right to consummate until 15 days. During this time, the parties who have interest in the merger can appeal.[96]

E. Fast-track Procedure, Indian Competition Law and the Green Channel Route

The main aim of the Green Channel Route is to avoid complications and promote the ease of doing business. However, the vagueness in not defining thresholds with respect to overlapping is moving this channel away from its main objective. Since combinations under Green Channel aim for zero overlapping, even a minute overlapping would also amount to gun-jumping and parties may have to face the consequences.[97] It may be argued that explaining the thresholds, as is done in the fast-track procedure available in Brazil, regarding the allowance of a certain percentage of combined market shares in horizontal and vertical overlapping, would erase the vagueness in this Route.

Additionally, it is known that as soon as the entities receive the receipt of acknowledgment from CCI, the combination may be consummated. As discussed above, another major drawback is the absence of a time limit for reviewing the combinations that took place through Green Channel. This may cause huge losses, if the entities already start operating. An example can be inferred from a recent scenario where a combination was filed under Green Channel Route in December 2022 by Platinum Trust, acting through Platinum Trustee, and TPG Upswing. They consummated in February, 2023 but CCI in August, 2023 declared it to be void and awarded penalties.[98] It is very important for CCI to recognise anti-competitive practices, but delay in this process may create chaos. Whereas, in Brazil, 30 days time is given to the GS to review the merger in fast-track procedure and another 15 days time to hear third party concerns.

Suggestions And Conclusion

The introduction of the Green Channel Route is a step in the right direction as it promotes ease of doing business and makes India one of the global champions of straightforward merger policies. However, it is important to keep in mind that the existence of such an automatic route, especially one that is vague in its procedures and processes, defeats the purpose of having such a route in the first place. Additionally, the Green Channel Route, as it exists now, may not align with the purpose of the Competition Act, 2002, which is to promote the economic development of the country.[99]

In order to ensure that the Green Channel Route is at par with international standards regarding accelerated merger procedures while ensuring the holistic economic development of the nation, references to South African and Brazilian competition law can be made. Firstly, the incorporation of the PIC test in South African merger control policy is a great example of inclusive economic development by a developing country. India may also allow for public interest to play a larger role in its competition policy in general as well as the Green Channel Route specifically. The addition of questions regarding how the proposed combination will impact public interest accompanied with a precise definition of the same may be added to Form 1. Secondly, the fast-track procedure as seen in Brazil is beneficial to both the competition authorities as well as merging entities. The inclusion of a prescribed time period within which the authority must look into the combination as well as clarity regarding the percentage of overlap allowed will increase accountability on the side of the authority and create more certainty for the combining entities. Therefore, a glance at foreign jurisdictions, with specific reference to developing economies, will aid India in making a better and safer Green Channel Route.

[1] Eleanor M. Fox, ‘Competition Policy: The Comparative Advantage Of Developing Countries’ [2016] 79 JSTOR <https://www.jstor.org/stable/45019871> 10 July 2023

[2] ‘Competition Commission of India, Government of India’ (Competition Commission of India) <https://www.cci.gov.in/combination/green-channel-view> accessed 2 August 2023

[3] ‘25% of M&As get CCI green channel nod’ The Times of India (Kolkata, 29 April 2023) <https://timesofindia.indiatimes.com/city/kolkata/25-of-mas-get-cci-green-channel-nod/articleshow/99858817.cms?from=mdr> accessed 20 July 2023

[4] Monopolies and Restrictive Trade Practices Act 1969 [hereinafter “MRTP Act”]

[5] Bhardwaj AK, ‘Introduction to Competition Law’ (Competition Commission of India, August 2016) <http://164.100.58.95/sites/default/files/advocacy_booklet_document/CCI%20Basic%20Introduction_0.pdf> accessed 27 July 2023

[6] Raghavan Committee, ‘High Level Committee on Competition Policy and Competition Law’ 66 (October 1999)

[7] The Competition (Amendment) Act 2023

[8] The Competition Act 2002 as amended by The Competition (Amendment) Act 2023 [hereinafter, “Competition Act”]

[9] ‘Notifications’ (Ministry of Corporate Affairs) <https://www.mca.gov.in/content/mca/global/en/acts-rules/ebooks/notifications.html> accessed 27 August 2023

[10] CCI (Procedure in regard to the transaction of Business relating to Combinations) Regulations, 2011 as amended by the Competition Commission of India (Procedure in regard to the transaction of business relating to combinations) Amendment Regulations, 2019 [hereinafter “2011 Regulations”]

[11] Competition Act, s 7(1)

[12] ibid, s 8(1)

[13] ibid, s 16(1)

[14] ibid, s 20(1)

[15] ibid, s 20(4)

[16] ibid, s 6(1)

[17] ibid, s 5

[18] ‘Competition Commission of India, Government of India’ (Competition Commission of India) <https://www.cci.gov.in/combination/combination/filing-of-combination-notice/introduction> accessed 14 August 2023

[19] ibid, s 5(d)

[20] ibid, s 6(2)

[21] 2011 Regulations, s 5

[22] Competition Act, s 6(2A)

[23] 2011 Regulations, s 19

[24] Competition Act, s 29(1)

[25] ibid, s 31(3)

[26] ibid, s 26(1)

[27] Competition Act, s 31(11)

[28] Injeti Srinivas Committee, ‘Report of the Competition Law Review Committee’ (July 2019)

[29] Competition Commission of India (Procedure in regard to the transaction of business relating to combinations) Amendment Regulations, 2019, w.e.f. 15-8-2019

[30] ibid

[31] Samir R Gandhi and others, ‘Merger Control in India: Overview’(Thomson Reuters Practical Law, 01 April 2022) <https://uk.practicallaw.thomsonreuters.com/0-5012861?transitionType=Default&contextData=(sc.Default)&firstPage=true#co_anchor_a707214> accessed 21 August 2023

[32] KR Srivtas, ‘Competition (Amendment) Act, 2023: Centre readies Rules to operationalise provisions’ The Hindu Business Line (18 July 2023) <https://www.thehindubusinessline.com/economy/competition-amendment-act-2023-centre-readies-rules-to-operationalise-provisions/article67090693.ece> accessed 21 July 2023

[33] Competition Act, s 5(4)

[34] ibid, s 5(5)

[35] ‘CCI’s Green Channel Approval – More Grey Than Green’ (Cyril Amarchand Mangaldas, 14 August 2019) </https://www.cyrilshroff.com/wp-content/uploads/2019/08/Client-Alert-CCI-Green-Channel> accessed 19 July 2023

[36] ibid, s 44

[37] Competition Act, s 43A

[38] Apurv Umredkar, ‘Green Channel Route: Resolving the Impediment and Procedural Infirmities’ (Kluwer Competition Law Blog, 28 June 2021) <https://competitionlawblog.kluwercompetitionlaw.com/2021/06/28/green-channel-route-resolving-the-impediment-and-procedural-infirmities/#:~:text=Procedure%20and%20Eligibility%20Criteria&text=That%20they%20do%20not%20manufacture,production%20chain%20(vertical%20overlaps)> accessed 17 August 2023

[39] ‘Investment flows to Africa reached a record $83 billion in 2021’ UNCTAD (09 June 2022) <https://unctad.org/news/investment-flows-africa-reached-record-83-billion-2021> accessed 18 August 2023

[40] The Competition Act 89 of 1998 as amended by the Competition Amendment Act 18 of 2018 [hereinafter “Competition Act 89”]

[41] Competition Act 89, Preamble

[42] ibid

[43] ibid, s 36

[44] Xolani Nyali and Lital Avivi, ‘Merger Control in South Africa: Overview’(Thomson Reuters Practical Law, 01 february 2022) <https://uk.practicallaw.thomsonreuters.com/2-504-5969?transitionType=Default&contextData=(sc.Default)&firstPage=true#co_anchor_a857035> accessed 21 July 2023

[45] Competition Act 89, s 12

[46] ‘Guidelines On Small Merger Notification’ Competition Commission of South Africa w.e.f 01 December 2022

[47] Ibid

[48] Competition Act 89, s 13

[49] ibid, s 14

[50] ibid, s 15

[51] ibid, s 12A(2)

[52] Paulo Correa and Frederico Aguiar, ‘Merger Control In Developing Countries: Lessons From The Brazilian Experience’ (2002) United Nations Conference On Trade And Development <chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=fdcbda037376f5555993d206189da762d006ae38> 18 July 2023

[53] The Competition Act (Law No. 12.529/2011) as amended by the Competition Act of 2022 (Law No. 14.470/2022) [hereinafter “Competition Act 2022”]

[54] Competition Act 2022, Art 2

[55] ‘Administrative Council for Economic Defense – CADE’ (Conselho Administrativo de Defesa Econômica) <https://www.gov.br/cade/en/access-to-information/about-us> accessed 3 August 2023

[56] Competition Act 2022, Art 4

[57] ibid, Art 5

[58] Tito Amaral de Andrade, Maria Eugênia Novis and Marcos Paulo Verissimo, ‘Brazil: Merger Control’(GCR, 19 September 2019) <https://globalcompetitionreview.com/review/the-antitrust-review-of-the-americas/2020/article/brazil-merger-control#footnote-004> accessed 23 July 2023

[59] Alberto Monteiro and Leonardo Maniglia Duarte ‘Spotlight: the merger control regime in Brazil’(Lexology, 06 August 2022) <https://www.lexology.com/library/detail.aspx?g=149d16e6-96c0-4012-bab2-b03888be9d72> accessed 19 July 2023

[60] Competition Act 2022, Art 88

[61] Leonardo Canabrava and others, ‘Merger Control in Brazil: Overview’(Thomson Reuters Practical Law, 01 January 2022) <https://uk.practicallaw.thomsonreuters.com/4-501-1911?transitionType=Default&contextData=(sc.Default)&firstPage=true> accessed 12 August 2023

[62] Competition Act 2022, Art 53

[63] ibid, Art 56

[64] ibid, Art 57

[65] ibid, Art 65

[66] ibid, Art 57

[67] ibid, Art 88

[68] CADE Resolution No. 33/2022 w.e.f April 2022

[69] Competition Act 2022, Art 88

[70] ibid, Art 36

[71] Mark A. Dutz and Maria Vagliasindi, ‘Competition policy implementation in transition economies: An empirical assessment’ [2000] 44 European Economic Review <https://doi.org/10.1016/S0014-2921(99)00060-4> 6 August 2023

[72] Bharat Vasani, ‘Indian Update – International Merger Control Regimes – It’s Time to Re-examine the Merger Control Regimes of India and other Emerging Economies’ (International Institute For The Study Of Cross‑border Investment And M&A, 6 February 2013) <https://xbma.org/indian-update-international-merger-control-regimes-its-time-to-re-examine-the-merger-control-regimes-of-india-and-other-emerging-economies/> accessed 15 August 2023

[73] ibid

[74] Competition Commission of India (n 18)

[75] ‘BRICS India 2021: Ministry of External Affairs’ (BRICS INDIA 2021 Ministry of External Affairs) <https://brics2021.gov.in/about-brics> accessed 7 August 2023

[76] Priest, George L., ‘Competition Law in Developing Nations: The Absolutist View’ (2013) 9 JSTOR 79,89 < https://doi.org/10.2307/j.ctvqsdzjf> accessed 23 August 2023

[77] Eleanor M. Fox, ‘Competition Policy: The Comparative Advantage Of Developing Countries’ (2016) 79 JSTOR 69,84 < https://www.jstor.org/stable/45019871> accessed 17 July 2023

[78] ibid

[79] EC Uwadi ‘A Case for Public Interest Considerations in Merger Control Analysis with Reference to Competition Law Enforcement in Developing Countries: The Example of South Africa’ (2020) TDM 1 <https://ueaeprints.uea.ac.uk/id/eprint/82861/1/Accepted_Manuscript.pdf > accessed 24 July 2023

[80] Competition Act 89, s 12A(3)

[81] ibid

[82] ibid, s 12

[83] EC Uwadi (n 79) 6

[84] Minister of Economic Development & Ors v. Competition Tribunal & Ors, 110/CAC/Jun11

[85] MRTP Act, s 38

[86] Competition Act, Preamble

[87] Aditya Bhattacharjea , ‘India’s Competition Policy: An Assessment ’ (2003) 38 JSTOR 3566 <https://www.jstor.org/stable/4413938> accessed 17 August 2023

[88] Competition Act, s 21 and s 21A

[89] ibid, s 59

[90] ibid, s 54

[91] Geeta Gauri , ‘Convergence of competition policy, competition law and public interest in India’ (2020) 6 Russian Journal of Economics 277, 293 <https://doi.org/10.32609/j.ruje.6.51303> accessed 18 July 2023

[92] 2011 Regulations, Form I

[93] ‘Brazil: CADE Formalizes 30 Day Term for Analysis of Mergers under Fast Track Proceedings: Perspectives & Events: Mayer Brown’ (Perspectives & Events Mayer Brown, 2016) <https://www.mayerbrown.com/en/perspectives-events/publications/2016/09/brazil-cade-formalizes-30-day-term-for-analysis-of> accessed 19 August 2023

[94] Tito Amaral de Andrade (n 58)

[95] ‘Quick Reference Guide: Brazil: Global Private M&A Guide’ Baker McKenzie Resource Hub <https://resourcehub.bakermckenzie.com/en/resources/global-private-ma-guide-limited/latin-america/brazil/topics/quick-reference-guide> accessed 31 July 2023

[96] Cristianne Saccab Zarzur Partner and others, ‘Merger Filing Guide: Brazil’ (Merger Control Guide – always up-to-date, 8 August 2023) <https://www.mergerfilers.com/guide.aspx?expertjuris=Brazil#guidebook> accessed 20 August 2023

[97] Apurv Umredkar (n 38)

[98] ‘CCI slaps Rs 55 lakh penalty on ADIA, TPG Group for false declarations’ Business Standard (New Delhi, 23 August 2023) <https://www.business-standard.com/companies/news/cci-slaps-rs-55-lakh-penalty-on-adia-tpg-group-for-false-declarations-123082300981_1.html> accessed 23 August 2023

[99] Competition Act (n 86)

(Impana Halgeri and Bokka Ashwika are law undergraduate at National University of Advanced Legal Studies, Kochi. The authors may be contacted via email at impana.h22.0@gmail.com and ratdeep02@gmail.com)

Cite as: Impana Halgeri and Bokka Ashwika,’ Merger Control In Developing Nations: Is Green Channel Taking India Through The Correct Route?’ 28 August, 2024<https://rmlnlulawreview.com/2024/08/29/merger-control-in-developing-nations-is-green-channel-taking-india-through-the-correct-route/> date of access.